Right now I have Laryngitis, I'm housesitting and the only people I will likely celebrate with tonight are Mom and Dad, right before I go back to housesitting. It's kind of ironic because I always assumed I'd spend this New Year's surrounded by lots of people, partying and about shouting my happiness, both figuratively and literally.

This is what I've been waiting for for more than three and a half years:

You can read the long and involved history about why this makes me so happy here.

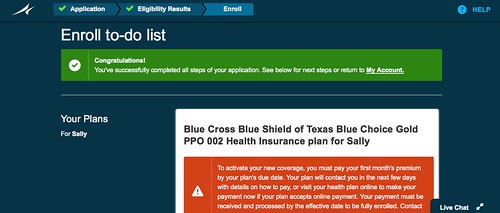

This screenshot was taken on December 21, 2013. Yes, I had difficulties with the website, although my father's multiple sources of income also made things difficult. (If you want to see if you qualify for subsidies, you have to enter household income information, including people in the household who aren't signing up for coverage.)

I was even part of the 2-5% of Americans (depending on whose counting) whose coverage was cancelled. (For that number, I suggest starting with this source: The Chart That Could Save Obamacare.) And I say good riddance to bad rubbish! Like all the cancelled plans, mine was substandard. The Texas Health Insurance Pool is a joke. Or should I say "was" a joke?

Since my COBRA ran out on March 1, 2012, the five or six expensive plans offered by the Texas Health Insurance Pool have been my only options. However, from Healthcare.gov, the Obamacare website, I was offered more than fifty. (The number may have been as high as the seventies. I don't remember the exact number, but there was a wide range of plans from bronze to platinum.)

I'm going to break it down for you. Please click the links to the glossary if you're confused. Keep in mind that I was a 33 year-old, non-smoking female until December 20, when I became a 34 year-old, non-smoking female:

Monthly Premiums :

Texas Health Insurance Pool: $486.00

Obamacare: $372.29

Annual Deductible :

Texas Health Insurance Pool: $3,000

Obamacare: $1,500

Annual Prescription Medication Deductible :

Texas Health Insurance Pool: $1,450

Obamacare: None!

Generic Drug Co-Pay :

Texas Health Insurance Pool: $10*

Obamacare:

* Some of my generic drugs cost less than $10 out of pocket, so in those drugs don't cost the full $10.

Cost of my most effective Pain Medication: (Estimates)

Texas Health Insurance Pool: No Coverage - I paid about $130.*

Obamacare: Coverage - a $35 co-pay maximum.*

*Full price is actually $210, but Robert the Pharmacist at my CVS gave me a discount card that saved me about $80 a month. It will probably save me even more when my insurance actually covers this drug. Robert, you are awesome!

Pregnancy Coverage:

Texas Health Insurance Pool: No!*

Obamacare: Yes!*

*Now exactly why was I paying so much more than a man for a plan with no pregnancy coverage?

Routine Eye Exam Coverage:

Texas Health Insurance Pool: No!

Obamacare: Yes!

Some of the other things are harder to compare. Like most high deductible plans, my Texas Health Insurance Plan had 100% coverage after I met that large deductible, while the Obamacare plan covers 80% after I meet the smaller deductible. (Of course, we're talking In Network Coinsurance.)

Long story short. I'm excited. I used my crappy plan for the last time today, at the doctor and at the pharmacy. When they asked me if my insurance I had changed, I said no, not for one more day. If I had more of a voice, I would have had a longer, louder talk about my new Obamacare plan.

Now some of you may be thinking, "Good for you, Sally, but I can't afford $372.29 a month! That's not affordable!" Before you blow it off, consider two things:

1. Subsidies!!!

There are tax subsidies available to help you pay your premiums. They are based on income. Anytime someone quotes you a scary sounding premium, ask them if that is before or after tax subsidies. Everyone forgets to figure in subsidies, including this lady.

Dad landed a pretty sweet gig recently, so we didn't qualify for subsidies at all. My premium is pre-subsidy. And it's still lower than my last premium.

2. You have lots of other options.

The plan I bought was a Gold plan, one of the most expensive. Even the Platinum plan cost less, but it had a very small network. There were many less expensive plans I could have chosen, but because I have multiple health problems, I chose a more expensive plan with more coverage. There are Silver and Bronze plans to choose from as well. And if you are under 30 or especially low income, you may be able to get a catastrophic plan, which is still a lot better than nothing.

I started 2011 in a lot of pain. In 2013 I got a work from home job. I think 2014 will be the year I finally move out. But it wouldn't have happened without my Obamacare plan.

Please share this far and wide. This is the stuff the media is missing.

You may hear me screaming at midnight after all.

Correction: I made an error when I first reported my generic drug co-pay. I originally thought it was $0 for all of them, but it turns out it's only $0 for preferred generic drugs, and $10 for the rest. However, I'm still saving quite a bit of money on my drugs.